Transforming Regulatory Fricition into a Seamless user anatomy Experience

In the high-stakes Fintech and iGaming industries, the "Closed Loop" policy is a non-negotiable anti-money laundering regulation. It mandates that users must withdraw funds back to their original deposit sources before claiming profits. Historically, our platform treated this as a manual, high-friction process. We believed that as long as the funds eventually reached the user, the manual intervention from our finance team was just a "cost of doing business."I directed the initial design strategy, treating the problem as a "Revenue Leak" and a "Trust Killer". Our initial interface was a static, sterile form that often left users confused when a withdrawal was partially denied or split across multiple cards. We were operating as "order takers" for legal requirements rather than designing for the human experience.

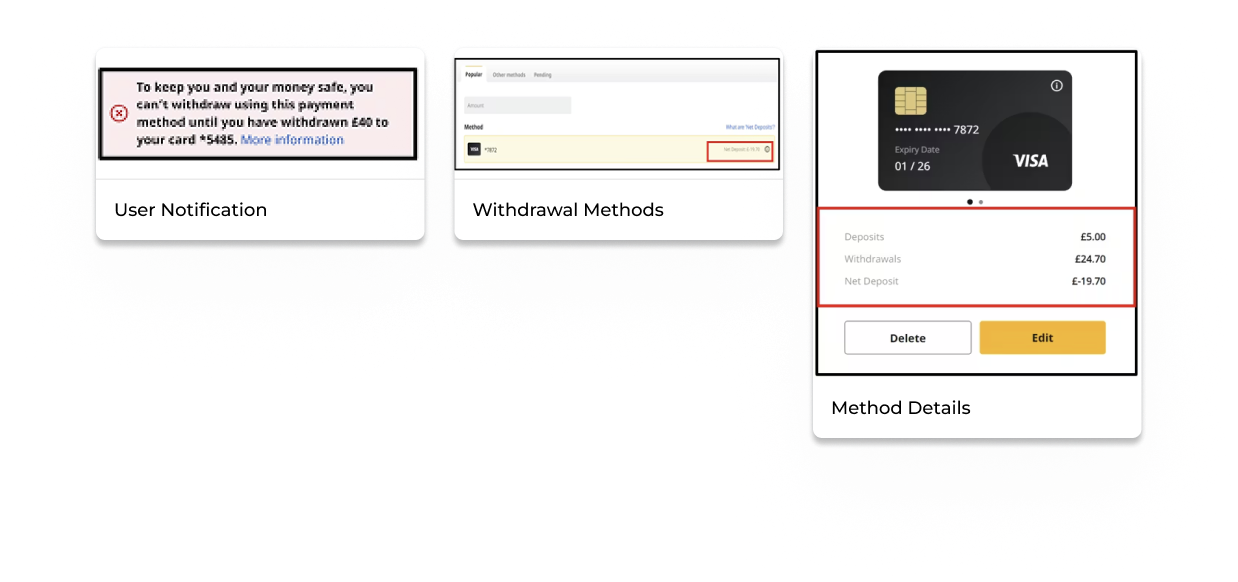

I looked for clues in our "Data Portrait" and analyzed the "Support Overhead Cost". The numbers were alarming: over 54% of withdrawals required manual back-office intervention. Users were met with generic "Something went wrong" error messages that failed to explain the regulatory "why" behind the friction.

This lack of transparency meant users felt policed rather than supported. The "Accepted Friction" of waiting days for a manual review was driving a 10% dip in user trust. I needed to find a way to turn a complex financial obligation into a manageable, transparent "task list" that users could complete themselves.

A small strike team gathered, and I facilitated an "Opportunity Scraper" audit of our backlog. Our hypothesis was to move "Upstream" into the planning cycle and design a 3-Tier "Smart Split" algorithm that could handle the logic in real-time.

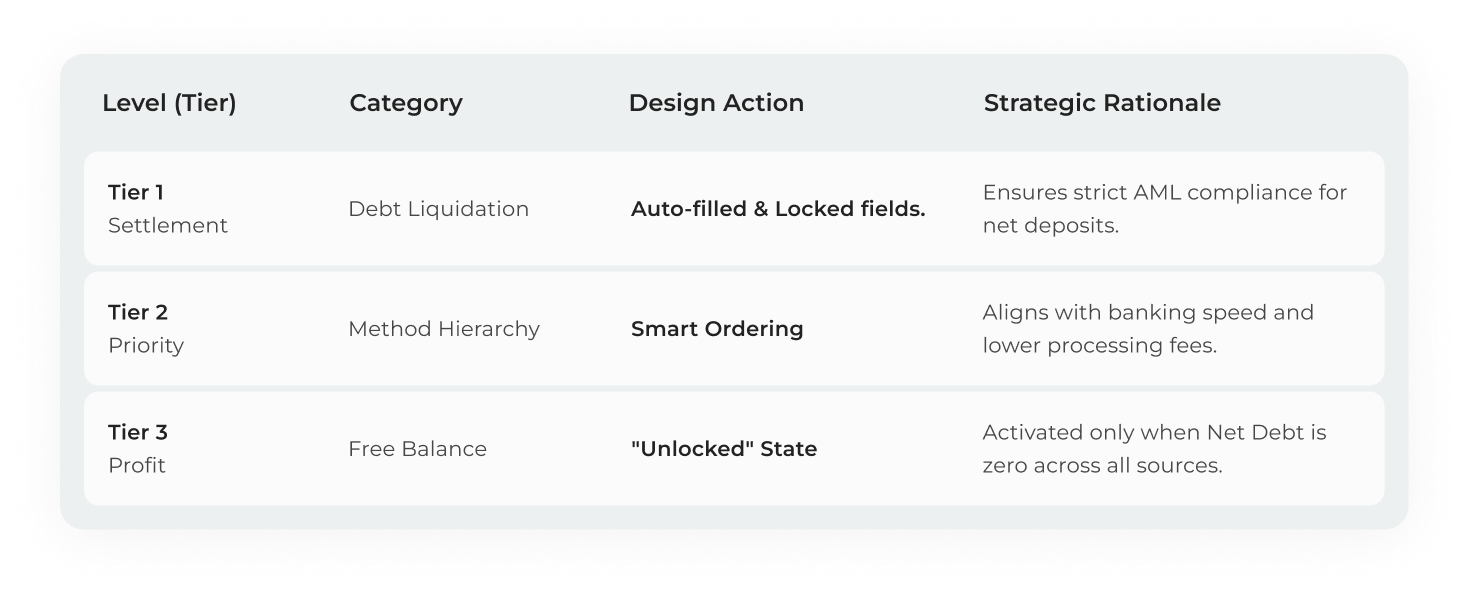

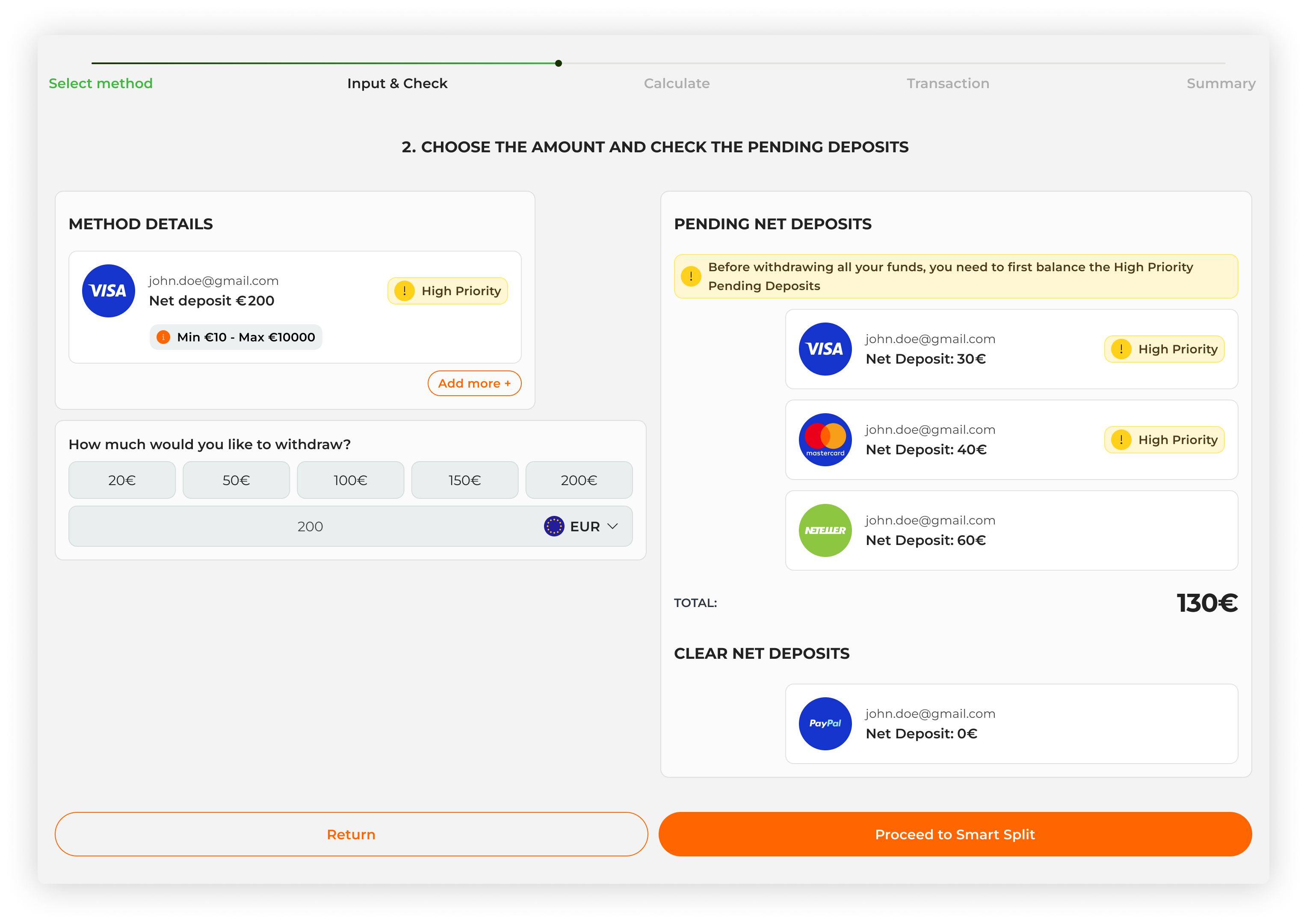

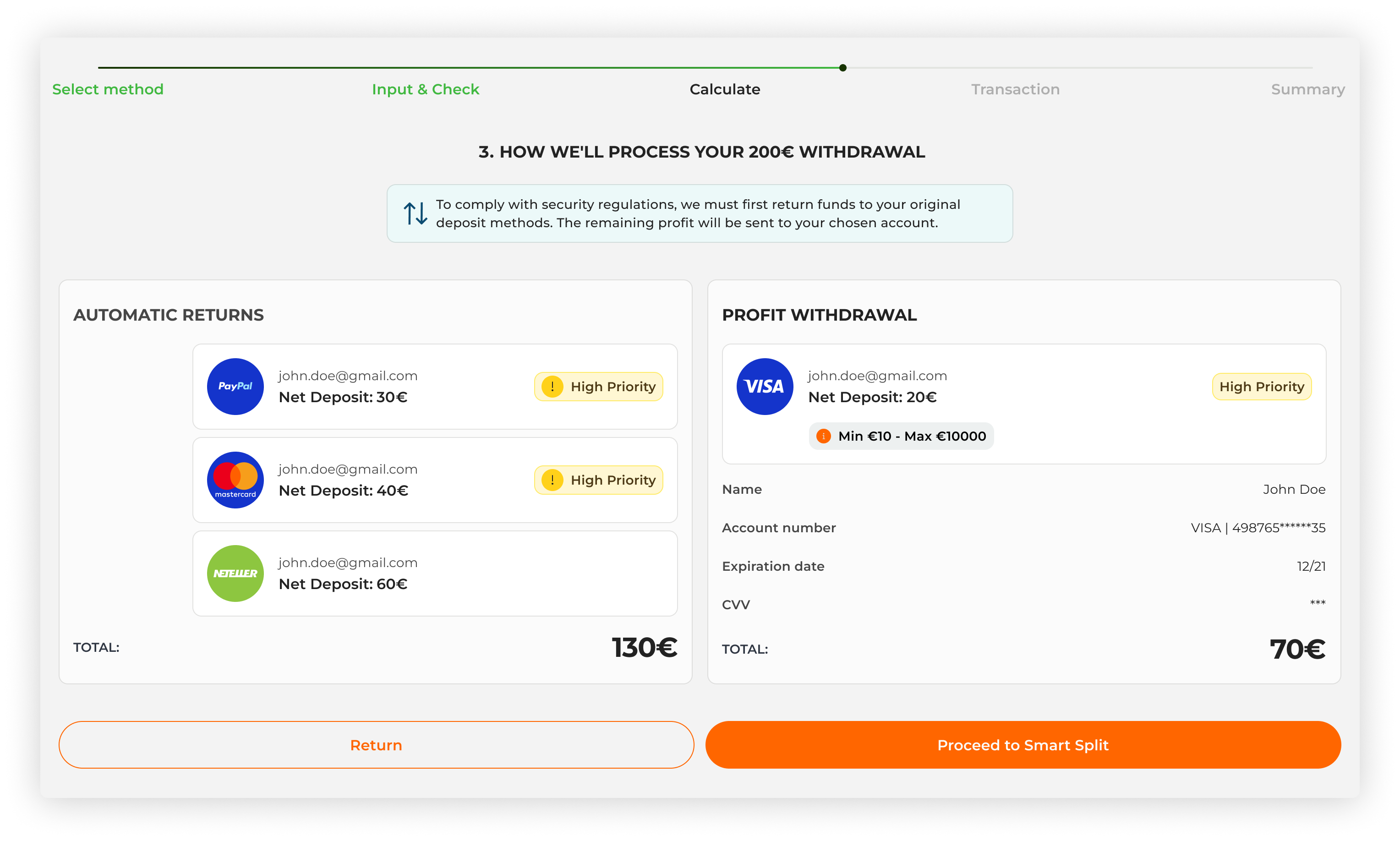

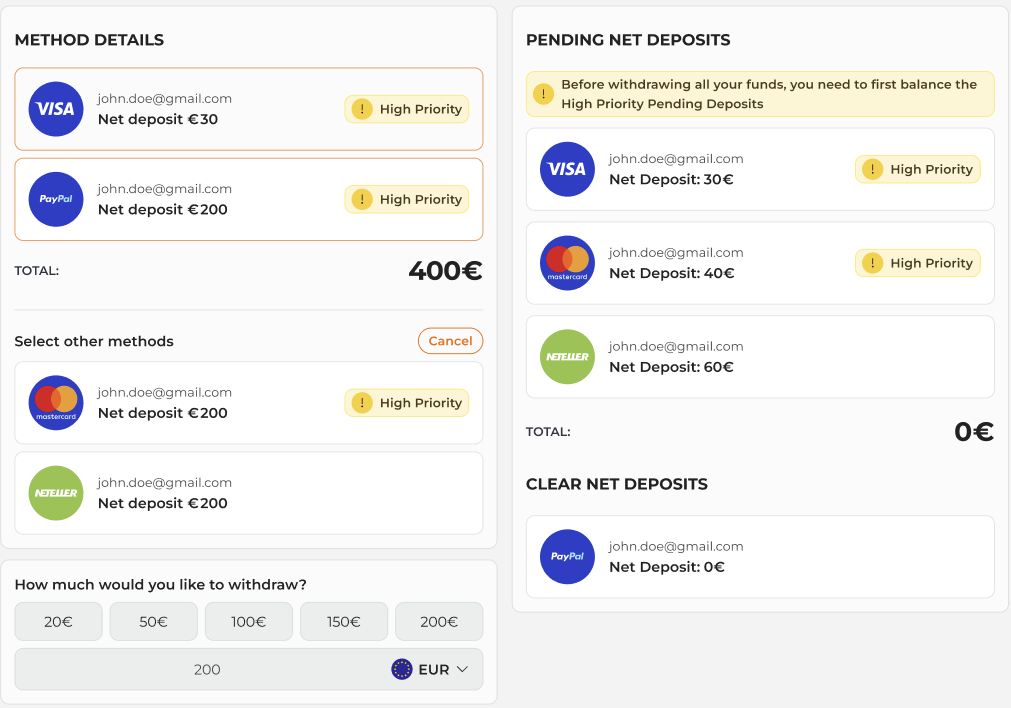

Armed with this vision, I architected a logic-driven system categorized into three levels: Tier 1 (Settlement), Tier 2 (Priority), and Tier 3 (Profit). Working with the Lead Engineer and QA, I delivered an "Edge-Case Blueprint" and a "Logic Matrix" to ensure the automation was 100% reliable even in complex scenarios where debt exceeded the current balance.

The service felt more like a financial tool than an entertainment experience. To break the cycle, I needed to engineer an “emotional moat” — a reason for users to stay that went beyond the next promotion.

“When we tested the Smart Spli calculator, users felt a sense of Proactive Resolution rather than frustation.”

— A strong signal that we were building an "Emotional Moat" around a previously sterile process

Finding traction and setting up scale

I rapidly adjusted our design system to support this new "Logic-First" architecture. Based on our "Disruptive Diagnosis," I identified three primary experience patterns to validate:

As a result of this strategic redesign, the platform moved from a high-friction manual process to an automated leader in the industry. We successfully surged automation from 45.6% to 85.7% and reduced the "Cost-per-Transaction" by 40%. We didn't just fix a form; we engineered a self-service engine that respects the user's time and trust.